EDITOR’S NOTE: We grow up. We grow old. We grow stronger and wiser. And sometimes we grow weary. In certain moments we grow closer. Other times we grow apart. How we thrive or falter depends on how we grow. At its roots is the idea of an abundant life for individuals, but also for communities and nations. Today, the Deseret News presents Part Three of Growing, an ongoing series.

SALT LAKE CITY — When Ashley LeBaron was 10, her parents thought she and her four siblings were acting entitled. So they pulled out the Monopoly money.

As the kids watched wide-eyed, they counted out how much they made each month, creating a stack that had the kids enthralled, LeBaron remembers.

To a 10-year-old, it looked like a LOT.

Then her parents started taking money off the pile. They subtracted the cost of housing, the expense of owning and running a car, the cost of lights and hot water and food, of clothing, of ... everything.

At the end, they had a bit left over, and their mom said they were blessed because lots of people don’t even have enough.

That was one of the first times LeBaron, who is now 23, really considered money, though it would not be the last. She’s now a family finance researcher at the University of Arizona.

Research says parents who shy away from discussing money and don’t teach sound principles may rob their children of future prosperity. It’s easier to learn and adopt good habits when you’re young.

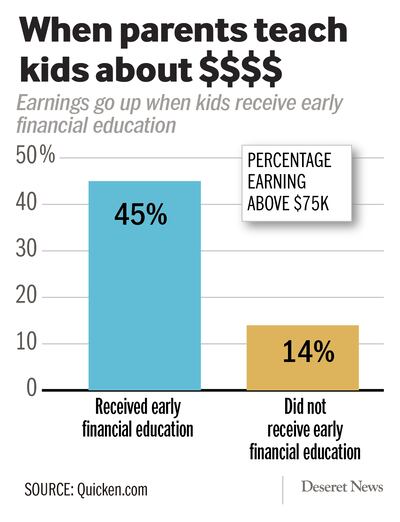

There’s a lot at stake: A survey by Quicken says reaching an income of at least $75,000 is challenging for adults who didn’t learn about money as children. And one-third of adults Quicken surveyed said they were not taught about money young. Those same adults are twice as likely not to talk about money to their children before 18, perhaps for lack of confidence.

At older ages, it’s harder to plant a prosperity mindset and adopt habits to back it up.

LeBaron’s research echoes that.

“Research has shown that the earlier children start forming attitudes, values and habits, the better off for them. ... Parent-child financial interactions really do impact them throughout their whole life, though I don’t want to say it’s ever too late to learn,” she said.

Why not teach

Since research confirms how vital it is to teach kids early about money and says parents are the most influential source of financial learning, why do so many avoid the topic?

LeBaron thinks some parents — especially those stressed financially — don’t talk about money because they don’t want to burden children with worries. They think they’re shielding them, but instead hurt them because the children don’t learn enough about money to use it well.

Discussing family finances also tempers expectations and helps children understand why others may have more. Parents can explain what is going wrong and brainstorm solutions, like conserving energy or not buying so many things or giving up activities for a while.

As for shielding them from worry, kids see parental stress, so it’s better to talk about it than let them imagine what’s happening, LeBaron said.

LeBaron led a study published in the Journal of Financial Counseling and Planning in 2018. It said the price of mismanaging finances goes beyond not building wealth and includes “poor health, academic stagnation, problematic interpersonal and family relationships and reduced likelihood of moving into adulthood effectively.”

On the other hand, parents who teach their kids principles and practices influence their children’s financial capability and independence. Their kids will have lower debt in emerging adulthood, more savings and better credit scores. They will be less likely to fall behind on loans including mortgages and will have higher net worth as adults. Good money management may even contribute to higher self-esteem, and better physical and psychological well-being, the study said.

The researchers found millennials are anxious to talk to their existing and hoped-for children about family finances, as well as about creating opportunities to learn financial responsibility by letting them handle money, the value of hard work and how to save.

Never too young

When kids are very young, in early grade school, parents should introduce basic savings and investing principles, explaining concepts in simple, understandable ways, said Dennis Pellegrini, a financial advisor at Peak Brokerage Services in Wyomissing, Pennsylvania.

“The earlier someone starts, the better,” he said. “That’s real simple math.’

By middle school and beyond, children should know that it’s better not to touch what they’ve saved. They should let it grow so they can buy something that’s important to them. “The key here is children understanding what the goal is — and the goal is to grow your assets,” said Pellegrini.

Just as adults should have an emergency fund, children need a separate account for short-term wants, like that great pair of sneakers. They can fund that and keep long-term funds safe, said Pellegrini.

The big challenge for older teens and college-age kids — a time when lenders and credit card companies are circling with enticing offers — is to avoid debt. Having the other principles in place when a child is young helps that greatly, said Pellegrini.

The best lessons target what a child responds to, he said. “Find out what their ‘why’ is. Not yours. Understand what makes them tick and appeal to that.”

A 2018 study by BYU researchers published in the Journal of Family and Economic Issues asked millennials, their parents and grandparents what they wish they’d been taught by their parents and what the parents and grandparents regretted about the way they passed financial wisdom to the millennials. Most of the “I wish” responses were about sharing practical knowledge, the importance of financial stewardship and having open communication.

Sometimes parents don’t know sound money principles themselves and don’t feel they can teach their children. Pellegrini said they should swallow their pride and get some coaching, for their own and for the children’s sake.

Where to begin

Loren Marks, a professor in the School of Family Life at BYU, has a starting point for teaching kids about finances. He says wise money management begins with being grateful for what you have and knowing the difference between needs and wants.

Money management should reflect a person’s values, as well, said LeBaron, but often doesn't. She said families should ask themselves what they care about when making money decisions and include it in the budget. For instance, if the parents’ relationship is important, budget for a couple getaway, a date night. Often, families don’t even have a budget.

E. Jeffrey Hill has 12 children and said the single best practice his family used to teach wise money management was the concept of a family bank, which he picked up from experts decades ago.

He and his wife were directors of the bank, which recently phased out when their youngest turned 18, said Hill, associate professor in the BYU School of Family Life. The children deposited money when they wanted and earned 10% interest a month, compounded monthly. They could borrow money, but the family bank charged 10% interest per month, compounded monthly. Every month, the bank directors reviewed with each child their balance, deposits and interest earned or paid. Hill said all but one of his children figured out that smart folks earn interest, instead of paying interest. The lesson was so successful they had to cap each family bank balance at $100 so the parents/bankers didn’t go broke. When a child reached $100, the money was deposited elsewhere.

One child, though, got so deep in debt they almost repossessed his cellphone before he caught on, Hill said. “He learned a valuable lesson.”

Gregg Murset, certified financial planner and founder of BusyKid, of Scottsdale, Arizona, taught his kids about money starting very early. The father of six said one son saved $10,000 by the time he left home at 21.

Murset uses everyday moments to teach. He knows kids pay more attention if they have to pay for something themselves, so he encourages them to buy dinner out, which definitely boosts awareness of how each item raises the bill. His kids learn to calculate tips, too.

In the grocery store, he might point out how much junk food costs and how little it rewards a person. Or explain the difference between credit and debit cards, which look the same.

A visit to the gas pump is a chance to discuss the cost of running a car, including the car itself, gas, tires, registration, insurance and oil changes, among other things.

Values matter in teaching about money. Murset said to teach work ethic and money smarts because the correlation between those two things and prosperity are clear. “If you teach those two primary things, you are setting them up for future success,” he said.

He has known a lot of parents who never taught their kids money concepts, either for lack of time or knowledge. That led him to create BusyKid, a chore and allowance platform. Parents subscribe, then children are given access to a real FDIC-insured account that lets them manage through the app how their allowance and payment for chores is used, with parental oversight. Children can even invest in shares of stock through BusyKid’s partnership with Stockpile.

Parents who don’t know where to start teaching their kids about money or who need some help with basics themselves will find a number of resources online.

For example, T. Rowe Price has put together a free Money Confident Kids activity guide to help parents and kids get started together. Parents can bolster and personalize the lessons by sharing their own stories about mistakes they’ve made along the way. According to the guide, “Your child can learn just as much from your missteps as your successes,”