In 1999, ABC introduced its hugely successful game show “Who Wants to Be a Millionaire?” At the time, the network felt no need to explain to America that being a millionaire was cultural shorthand for being rich and successful. Everyone knew that getting a million dollars was a game changer.

But these days, a million dollars has become more ordinary — not just something that happens to game show winners, star athletes or celebrities. Indeed, a million dollars in assets will facilitate a comfortable retirement, but by no means a lavish one.

For the many who are struggling to make ends meet, the idea that millionaire status has become increasingly common may be hard to fathom. Which households are meeting that standard, anyway?

Millionaire status is common but uneven

To explore this question, we used a leading source of data on the financial status of U.S. families, the Survey of Consumer Finances, collected every three years by the Federal Reserve Board.

In 2022, the average family net worth in America was $1.05 million, but that figure includes a lot of very wealthy people. The typical family (the statistical median) had a net worth of only about $192,000. This difference illustrates the large — and growing — level of wealth inequality in America today.

Data also shows that about 18% of American families had a net worth of at least $1 million in 2022, a share that has risen steadily over time. By comparison, adjusting for inflation, less than 11% of families in 2001 would qualify as millionaires.

Marriage and wealth

Extensive research has identified multiple forces that drive wealth accumulation. Higher education is arguably the primary driver, but occupation and geography also play a role. The start individuals get in life in terms of parental wealth is also key.

All these variables get plenty of attention in modern discourse. But one basic component of wealth accumulation is sometimes neglected, and may be a surprise to many: marriage. In our analysis, we asked how married couples fare in the data compared to unmarried — those who haven’t married or had their marriage end through divorce or death.

Across all ages, about 25% of married families were millionaires in 2022. Among families that were not married, the share drops to only about 9%.

Among other things, this significant difference reflects the advantages gained by pooling resources through marriage and avoiding the division of shared assets through divorce.

This difference becomes even larger later in life. Among families headed by people ages 55 to 74, nearly 38% of married families had a net worth above $1 million. For nonmarried families in the same age range, only about 15% reached that threshold.

The basic advantage of marriage, once again, is a result of the fundamental law of household economy: Two people can live more cheaply together than they can apart. Add to that the advantage of two earners contributing to the same financial pot (in cases where both spouses are employed) and we see a widening advantage of married families over nonmarried families.

Marriage also creates a schoolhouse for creating habits and virtues — discipline, compassion, sacrifice, patience, to name a few. These, in turn, have a payoff not only in creating successful marriage and family but also in becoming habits that promote wealth accumulation.

A strong marriage that is financially secure is also in a position to help the next generation and to contribute meaningfully to the community. Thus, sheer dollar comparisons reflect only a part of the social value of marriage.

Marital status in later life reflects a combined lifetime of forces, both positive and negative. Adverse health shocks, job loss, failed investments and the ordinary stresses of life can strain or end marriages. In that sense, economic stability influences the preservation of marriage just as marriage influences economic outcomes.

Social inequalities and wealth

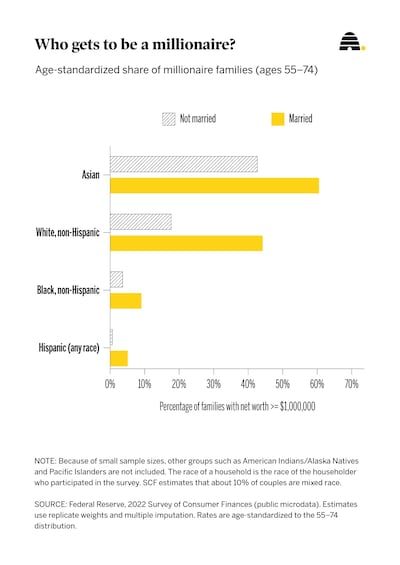

This effect of marriage is universal across differing American communities. Married households of all racial groups are much more likely to be millionaires than their unmarried counterparts.

This belies the notion that marital advantage is simply a feature of “white privilege.” Married people of all races are doing better financially than their single counterparts.

The story of race is not a simple one. For instance, Asians are doing the best financially of all.

Because communities in America have sharply different rates of marriage (among those 55-74, 71% of Asians, 66% of Hispanics, 58% of white people and only 44% of Black people are married), some have wondered if differences in marriage drive racial wealth gaps.

They do not. If we only look at the married group in a comparison of households by race, the millionaire rate is 61% for Asians, 44% for white people, 9% for Black people and 5% for Hispanics. Thus, even if everyone were married, profound racial disparities would still likely exist.

An empowering decision

Marriage does not erase racial wealth gaps. Deeply rooted social inequalities remain. But family stability is consistently associated with higher wealth accumulation for all racial groups.

The choices people make over their lives determine wealth accumulation. One important choice is the decision to get — and stay — married.

But again, social and economic conditions, such as those caused by structural inequalities tied to race, also have a profound impact. We think a worthy goal is to better understand both the individual choices and social conditions leading to greater financial security for all American communities.