Last in a three-part series

Linda Hilton, an advocate for the poor, abhors "payday loans."

On average, they charge 521 percent annual interest in Utah. Some charge nearly 1,000 percent. And Hilton says she has seen too many people forced into bankruptcy or homelessness by them.

So, she thought lobbying the Legislature, for example, to cap interest at the still-stratospheric rate of 500 percent would be an easy sell. "Boy, was I wrong," she said.

Hilton says she found payday lenders have powerful friends: "mainly, the whole mainstream financial industry," she said. "Bankers up there told me, in so many words, that we would be opening Pandora's box. They said if we capped payday loan interest, then someone might want to cap bank loan interest or mortgage rates, too."

She and her allies also were told that Utah attracts many "industrial banks" (operated by commercial companies such as American Express, General Motors and Merrill Lynch) that bring thousands of jobs to Utah. Lawmakers worry that anything that weakens Utah's wide-open, let-the-market-rule financial laws might scare them and their jobs out of state.

Hilton also says that while advocates for the poor lobby in the Capitol hallways, the financial industry was often invited into the back rooms for far better access. That comes as the financial industry gives more to the Legislature than any other special-interest group. It donated $1 of every $8 that legislators raised in the past election.

While Hilton and her allies have pushed bills for years to try to impose some of the tighter payday loan regulations found in other states, only a few relatively minor provisions have passed here. Most bills do not even come close to passing through committee.

Hilton says she and her allies plan to try yet again at the next Legislature. But both she and her opponents figure she has only a long-shot chance, for a variety of reasons — all of which continue to make Utah a home sweet home for payday lenders.

Friendly Utah

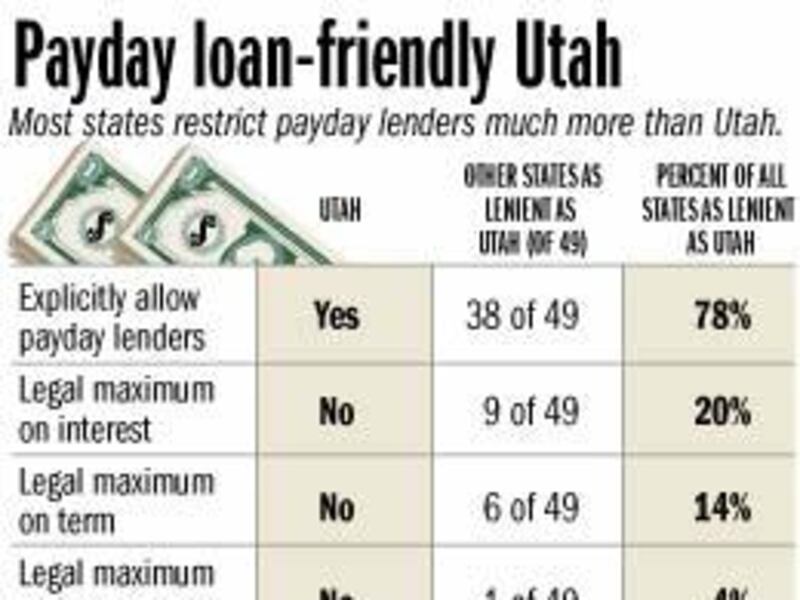

Few states have friendlier laws for the payday loan industry than Utah — which the industry and its allies would like to continue but which critics want to change.

Utah is among 39 states that explicitly allow such loans. It is among only 10 that have no cap on their interest rates or fees. It is among two with no legal maximum for such loans. Utah also allows among the longest periods to "roll over" loans with continuing high interest: up to 12 weeks. Most states ban rollovers.

Among the 39 states that explicitly allow payday loans, 23 cap interest at rates that are lower than the median now charged by lenders in Utah: 521 percent annually. A median means half charge that amount or less, and half charge that amount or more.

So, half or more of Utah's payday lenders charge rates so high they would be banned in many states.

Utah did not regulate payday lenders at all until 1998. Regulations adopted then were fairly minor: Lenders must apply for a license; they may extend loans only for 12 weeks (meaning they are interest-free after that, but the lender can impose a variety of collection fees); and they must provide written contracts listing annual interest rates.

They must also post on signs their rates, both as an annual percentage rate and as a dollar cost. They must post signs with the phone numbers of state regulators, with whom customers could file any complaints.

As shown in the first part of this series, Morning News visits to 67 lenders showed about a quarter of them failed to post required signs. Several also gave misleading statements about interest rates to a reporter asking about loans.

Hilton complains that state law provides no financial penalties for payday lenders who violate regulations or mislead borrowers — and that inspectors do not perform any undercover inspections that could catch any deception used on borrowers.

However, Jerry R. Jaramillo, a supervisor in the Utah Department of Financial Institutions who oversees inspections of the industry, says the state can close any payday lenders who have too many violations or complaints. It has closed only one through the years, however.

Industrywide concern

As Hilton and others tried to toughen regulations on payday lenders, it set off alarms for banks, credit unions, industrial banks and others that worried it could also lead to interest caps and tougher regulation of them as well. They tried to keep the battle front far away from where it might hurt their businesses, which charge much lower rates.

Rep. Paul Ray, R-Clearfield, who works for a bank, is another who verifies that the entire financial industry expressed concern.

"If the Legislature caps one area, it might also lead to a cap on mortgage rates or a cap on car loans or credit card rates," he said about the industry's worries.

Frank Pignanelli tells how industrial banks reacted. He is a lobbyist for them. While most states do not allow commercial companies to own or operate banks, Utah does allow "industrial banks" owned by groups ranging from General Motors to Merrill Lynch and Volkswagen to make loans and take deposits nationally. Utah has become a haven for them, creating thousands of jobs.

Pignanelli said when "usury limits were proposed, it brought out everyone in the industry."

He says they asked him to work with payday lenders to find reasonable regulation and avoid interest caps.

So, Pignanelli also became the attorney, lobbyist and spokesman for the payday loan industry's Utah Consumer Loan Association.

"I was hesitant at first, because I had heard horror stories that these were bad people who charged high rates. But when I looked into it, I found it was a good industry," he said.

Arguments

Pignanelli says payday lenders must charge high interest because they are dealing with people with poor credit whose loans are not secured. He says companies need to cover the costs of loan processing and make a profit. He says any interest rate cap that falsely manipulates market demand could put many of them out of business.

Hilton scoffs at that assessment.

"There are many states with caps," she said. "Not only have payday lenders there not gone out of business when those laws passed, but the number of outlets in the states continues to grow. . . . They are making money."

Christopher Peterson, a native Utahn who is a University of Florida law professor and an expert on the high-credit industry, says states always imposed usury caps until recent decades — and Utah abolished its usury cap only in the early 1980s.

Further, Hilton scoffs at mainstream banks worried that a cap of 500 percent or so targeted at payday lenders could also hurt them.

"They don't charge interest anywhere near that high," she said. "They just worry it might make someone decide that since one interest rate was capped that, gee, maybe it would be good to also cap mortgage rates and other bank loans, too."

But Pignanelli says even the perception that Utah is becoming a little more unfriendly to the financial industry could have dire consequences.

"If the state puts a usury cap on, it is a signal that the state is unfriendly to financial institutions," he said. "It could lead to industrial banks going elsewhere."

Also, if payday lenders are put out of business, he says their current customers would end up instead paying high bounced-check fees, utility reconnection charges and other fees costing more than current loans.

"So, it would hurt everybody," he said.

Pignanelli also charges that most people who use payday loans are satisfied with them and that critics falsely make it sound like high numbers are pushed into bankruptcy or other problems by such loans.

Pignanelli says a survey conducted for the industry in Utah last year shows 77 percent of payday borrowers were satisfied with their loan experience.

Former Sen. Ron Allen, D-Tooele, now a member of the Public Service Commission, says the perception that few victims exist hurts some bills he sponsored calling for tougher payday lender regulations. He said: "When we had hearings, no victims would show up. Many are working poor and could not take off work to come. Others are likely embarrassed."

He says repeated failure of victims to testify prevented putting "a human face on the problem" and reinforced industry arguments that few people have trouble with the loans.

Ray, the House member from Clearfield, says he also pushed some bills to restrict payday lenders but backed off when he couldn't find many victims. His district includes Hill Air Force Base, which Morning News analysis shows has 28 payday lenders nearby. He said he had heard stories about military members hurt by them.

"But I couldn't find any," he said.

Hilton says victims are real and are seen by many churches she works with as coordinator of the Coalition of Religious Communities. She says she can connect many with lawmakers who want to hear stories — and is using college students to compile a book of their stories to help overcome such criticism.

Debt counseling services also say they see many people driven to severe financial crisis by payday loans. Don Hester, co-owner of the Debt Free Consumer counseling service in Provo, says his records show a 400 percent yearly increase in the number of clients who had payday loan problems — and 15 percent of all clients have some.

When Preston Cochrane, executive director of the AAA Fair Credit Foundation, is asked whether the number of clients with payday loan problems was low, medium or high, he says high.

Well-connected allies

Hilton says a main problem faced by critics of the payday loan industry is that its allies in the financial industry are well-connected.

The financial industry donated nearly $345,000 to legislators in the last election, or $1 of every $8 they raised, Morning News analysis of campaign records show. That was the most of any special interest. Almost every legislator received some money from the industry.

Something else that helped access by payday lenders, Hilton says, was the election of one payday lender to the Legislature. Former Sen. James Evans, R-Rose Park, who is now chairman of the Salt Lake County Republican Party, owns the Check Line, Check Action and Rainbow Check Cashing payday lending businesses.

"He did everything he could to undo all of our work," she said.

She says Evans was able to bring lobbyists for his industry into the back rooms to meet with fellow legislators.

"I can tell you that with him in the back room and us out in the hall, we didn't have a chance," she said.

Allen, the former senator from Tooele, said, "Some of that happened, but I don't think he had as much power as she thinks."

Pignanelli, the lobbyist for the industry, says it didn't happen at all — and that he and others working with the industry made a point to try to keep Evans at a distance on any legislation affecting it because such criticism could arise.

Evans initially did not return phone calls seeking response. But when he visited the Morning News editorial board to attack Salt Lake City Mayor Rocky Anderson about use of taxpayer money on his trips, Evans was asked about his role in payday loan legislation. He became furious but denied any improper influence.

"Anytime I go after any liberal cause this comes up. . . . That's the only thing this segment of the political spectrum can utilize," he said. "If you detect some hostility, there is. . . . It's almost like a 'have you stopped beating your wife' setup. I mean, some of these accusations, I no longer respond to."

Evans also says the industry's Utah Consumer Lending Association — of which he is not a member — has asked him not to talk to the press about payday loans and to refer inquiries to Pignanelli. Evans declined to respond to questions about how he built his business and how much profit it makes now.

Proposals

Because of stiff opposition to caps on interest rates from the financial industry, Hilton says she and her allies do not plan to push that again anytime soon. But she says they may have several other bills at the next Legislature proposing other sorts of tighter regulations.

"I would like to see some financial penalty for violating state regulations," she said. "Now if they (lenders) break the law, one of two things happen: (1) Nothing; or (2), if it's bad enough, the state shuts them down. There is nothing in between."

She would also like to fix a problem with a law that gives borrowers 24 hours to cancel a loan without penalty. The problem is that current law does not require lenders to tell borrowers about that provision, and she thinks it should.

Hilton would also like to outlaw allowing wage garnishment by payday lenders. (Now it is allowed only if a borrower voluntarily agrees to it — and they may revoke that at any time. However, some lenders seek that permission before they approve loans.)

"We've heard a lot of garnishment horror stories," she said.

Also, she says she would like to see Utah establish a central database that payday lenders would have to check to ensure that borrowers do not have other payday loans outstanding — which some states do. It would help prevent them from taking out more loans than they can afford.

And Hilton says she would like a law banning payday loans to potential borrowers who exceed a certain debt-to-wage ratio, suggesting they cannot afford the loan. However, Jaramillo says state regulators frown on that and says the state likely should allow people to decide for themselves whether they can afford a loan.

Among lawmakers who said they are considering bills to restrict payday lenders in some way are Reps. Patricia Jones, D-Salt Lake, and Lorie Fowlke, R-Orem.

Pignanelli says the industry does not oppose reasonable regulation — and sometimes has pushed for some itself to rein in "bad apples."

He says that included last year agreeing to steps to stop some lenders who were obtaining civil judgments that forced borrowers to continue to pay triple-digit interest until loans were fully paid. The industry, he says, has agreed to live with the 12-week cap on such interest.

R. Paul Allred, deputy commissioner of the Utah Department of Financial Institutions, says state regulators also will have some suggested legislation dealing with payday lenders. However, he says it is premature to discuss publicly what they might be because regulators have not found sponsors for their provisions.

Some others would like to see steps that many say are politically impossible for now.

Peterson, the University of Florida law professor, suggests that Utah restore the interest rate caps that it had until the early 1980s, saying it would be the best way to ensure against gouging the unwary.

"What's happened in the past 25-20 years (in erasing such caps) is a radical and unconventional shift in the law that is not the historical conservative position," he said.

Hester, co-owner of the Debt Free Consumer counseling service, uses bold words to say he thinks the industry should be reined in very tightly.

"It is unconscionable that the state of Utah allows these companies to operate with impunity," he said. "The annual percentage rate allowed to be charged on payday loans should be capped at 30 percent APR. These loans should not be eligible to be rolled over or replaced by a second loan. Our citizens need to be protected from these scavengers. It is time the legislators of Utah address this wanton financial rape of our citizens."

E-mail: lee@desnews.com