Our economy has long relied on an optimistic, intrepid bunch of business explorers willing to risk time, treasure and mental health on some new idea. The nation calls them entrepreneurs and the businesses they launch "startups."

The government calls them "business establishments less than a year old." While many of them fail, some persist and eventually grow into long-term, growing businesses that help families prosper. With this entreprenuerial income, parents pay for mortgages, braces and tuition.

Some startups are sold to other investors or larger businesses. They are often the source of our most important innovations. But they have lost their vitality.

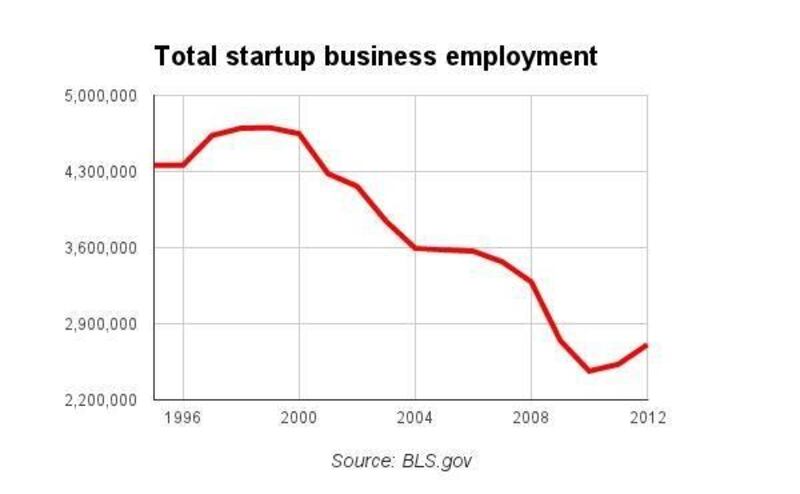

In the past, the U.S. economy has depended upon these market adventurers as sources of new employment. But recent years haven't been so favorable to small business startups. In a little over 15 years, employment has fallen by almost half, peaking in 1999 at 4.7 million, while only generating 2.7 million jobs in 2012.

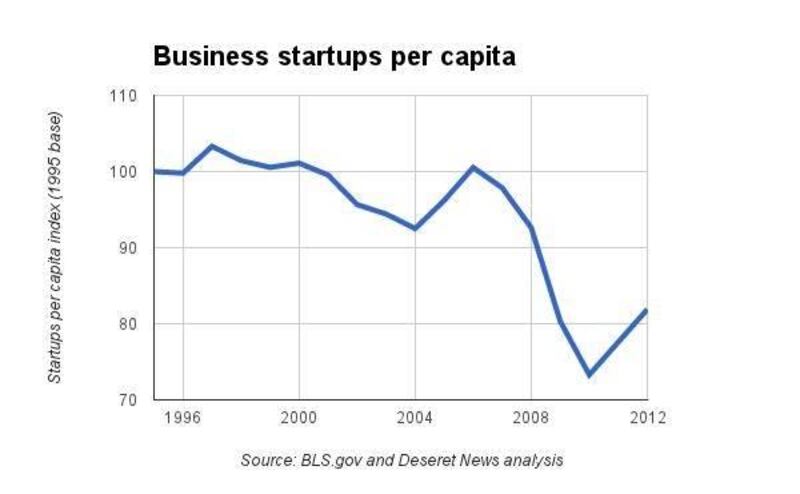

Perhaps even more troubling is that our ability to launch and develop successful small businesses is falling behind population growth. Using 1995 as a base, startup business employment per capita or per population has fallen 20 percent. In other words, our ability to build new businesses is not keeping up with year-over-year population growth.

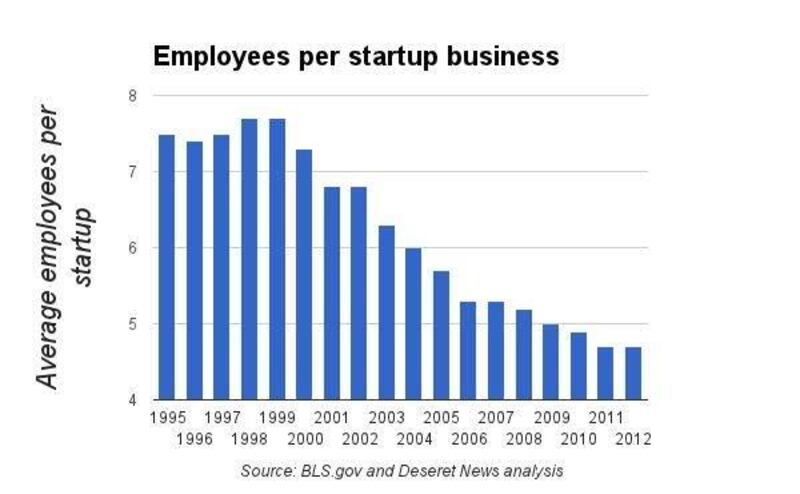

In yet another view of the data we see that the number of employees per new startup has fallen from a high of 7.7 employees in 1999 to 4.7 in 2012. So, entrepreneurs are hiring three fewer employees on average during their initial year of business.

But why the decline of the American entrepreneur? State and national politicians are quick to point the finger of blame at one another for failure to pass one program or another. Others point to the recent real estate implosion. Others explain away the falling employment through increased efficiencies. But it is clear that startups have been trending down for some time.

Let's look at this issue from the view of the entrepreneur. Fundamentally, when people look at business opportunities, they look at ceilings and floors. The ceiling represents revenue potential while the floor is the cost of pursuing it. So, when a person decides to leave a job to launch a new business, or start one on the side, it is typically because the space between the ceiling and the floor, also known as profits, is big enough to warrant the risk.

Startups are risky propositions to begin with, no matter how potentially profitable the idea. The basic resources available to entrepreneurs are time, money, know-how and labor. These resources also make up the cost or floor of the business.

Now lets frame government intervention from the point of view of the entrepreneur.

First, taxes affect the ceiling or revenue potential for the new business. Increased taxes lower the ceiling, or opportunity, leading many would-be business creators to abandon or modify their course.

Second, government debt increases the cost of working capital or borrowing for small businesses, raising the floor. Businesses use working capital to bridge between making something and selling it. Economists have long argued that when government borrows money, it "crowds out" or competes with private business borrowers vying for capital. Startups usually see the effects as raised interest rates or elevated credit qualifications.

Third, government regulations also raise the floor by increasing the time cost of compliance. Among all resources available to small business owner, perhaps the most precious is time. While reasonable regulations aid markets and transactions, recent dramatic growth in regulatory oversight have been particularly damaging to small businesess unable to absorb the costs of compliance.

In a recent interview, Subway founder Fred DeLuca explained that, "Subway would not exist," if he tried to start his business today due to the regulatory environment and cost of doing business.

The heartbeat of the American dream is the potential of turning risks into rewards. But as we lower ceilings and raise floors, the room for the entrepreneur and the family business is getting ever smaller.

Matthew studied economics at BYU and business and government at Harvard. He is GM of Deseret Connect and Deseret News Service at Deseret Digital Media. Follow him on Twitter @Sanders_Matt or subscribe to the Reframing the Debate email feed.