The nation’s home prices have skyrocketed, shattered records and continued upward with no real plateau in sight. But now some national researchers and economists are warning they are seeing signs of a housing bubble brewing.

It’s not the same as the last housing bubble that preceded the market crash and global financial crisis in 2007 and 2008.

“However, there is growing concern that U.S. house prices are again becoming unhinged from fundamentals,” researchers and economists at the Federal Reserve Bank of Dallas wrote in a blog post published Tuesday.

Until recently, experts haven’t widely supported the possibility of a housing bubble about to burst, especially in states like Utah, where demand continues to woefully outpace supply despite record price increases.

But now, federal researchers are warning of “abnormal” U.S. market behavior that points to signs of a U.S. housing bubble — though they don’t predict if or when it would pop.

But there is some good news.

“We argue that the underlying causes of the run-up differ from those during the last housing boom” that preceded the Great Recession, researchers wrote.

If you’re thinking about the global economic crisis that followed the 2007 bubble burst, researchers said there’s “no expectation that fallout from a housing correction would be comparable” to that crash “in terms of magnitude or macroeconomic gravity.”

“Among other things, household balance sheets appear in better shape, and excessive borrowing doesn’t appear to be fueling the housing market boom,” researchers wrote.

Importantly, they added, experience from the housing bubble and the Great Recession led to development of “advanced tools for early detection and deployment of warning indicators.” That means “market participants, banks, policymakers and regulators are all better equipped to assess in real time the significance of a housing boom,” they wrote.

“Thus, they are in a more informed position to react quickly and avoid the most severe, negative consequences of a housing correction.”

The researchers said they used a real-time market monitoring statistical tool kit for assessing the health of the U.S., in partnership with “networks of scholars from around the world” collaborating under the International Housing Observatory. The methodology, they wrote, uses “novel statistical methods to continuously monitor housing markets ... to detect symptoms and signal the presence of emerging housing booms.”

What does this mean for Utah’s housing market?

Dejan Eskic, senior research fellow at the University of Utah’s Kem C. Gardner Policy Institute who specializes in housing research, told the Deseret News on Thursday that Utahns shouldn’t panic or jump to hasty conclusions from the new report.

He said the typical understanding of a “bubble” — or what Americans saw in 2008 — is not the same as what’s happening in today’s market, where there continues to be a real demand in housing, especially in Western states like Utah.

“My pushback on it is what’s driving the growth in housing prices is the lack of inventory,” he said.

In the 2000s, when the U.S. had overbuilt housing and there was a subprime mortgage crisis depicted in such films as “The Big Short,” Eskic said “everybody and their dog was getting mortgages.”

Today, Eskic said, it’s not easy to get a home loan.

“Incomes are solid, too, for homebuyers,” he said. “The people that are buying, they can afford it. Lending (requirements) got tighter, so you really have to go above and beyond” to qualify.

Plus, there’s not as much market speculation in Utah’s market, Eskic noted. While some areas such as Atlanta and Arizona are seeing investors make up about 40% of their housing markets, in Utah investors only make up about 15%, he said.

“So our market is driven by real people wanting housing,” he said.

Utah continues to see extremely low inventory with price increases driven by demand, so it’s hard to fathom a bubble popping in the foreseeable future, Eskic said.

“For a bubble to pop, in my opinion, you need oversupply,” he said. “It’s not a stock that people get frenzied into and all of a sudden it disappears. We’re talking about real physical assets that are occupied by people.”

So what should Utahns take away from the national research warning of signs of a bubble? Proceed with caution, Eskic said.

“It all depends on what your goals are,” he said. “If you are an investor, now is a really shaky time to invest.”

He noted rising interest rates have pushed prices even higher, pricing even more people out of the market.

“It’s an important thing not to overreact on any given part of the economy,” Eskic said. “Things go south when we overreact in a short time frame. That’s when things can really pop off.”

Eskic noted household economics do continue to appear strong, pointing to job growth in Utah and across the U.S.

“For prices to really crash,” Eskic said, “you need some black swan economic frenzy event and people can’t make their monthly payments.”

Is a bubble emerging?

Researchers wrote an asset, like housing, is in the “primary expansionary phase of a bubble when price increases are out of step with market fundamentals.” Rapid price increases alone “does not in itself signal a bubble.”

However, house prices can “diverge from market fundamentals,” researchers wrote, “when there is widespread belief that today’s robust price increases will continue.” If most buyers believe prices will continue to go up, “purchases arising from ‘a fear of missing out’ can drive up prices and heighten expectations” of continued price hikes.

That leads to price growth that may become “exponential” or even “explosive,” researchers wrote, “resulting in the housing market becoming progressively misaligned from fundamentals until investors become cautious, policymakers intervene, the flow of money into housing dries up and a housing correction or even a bust occurs.”

Those “expectations-driven, explosive” price increases, which researchers wrote is “often called exuberance,” has consequences, including “misallocation of economic resources, distorted investment patterns, individual bankruptcies and broad macroeconomic effects on growth and employment.”

Signs of a market ‘tipping point’

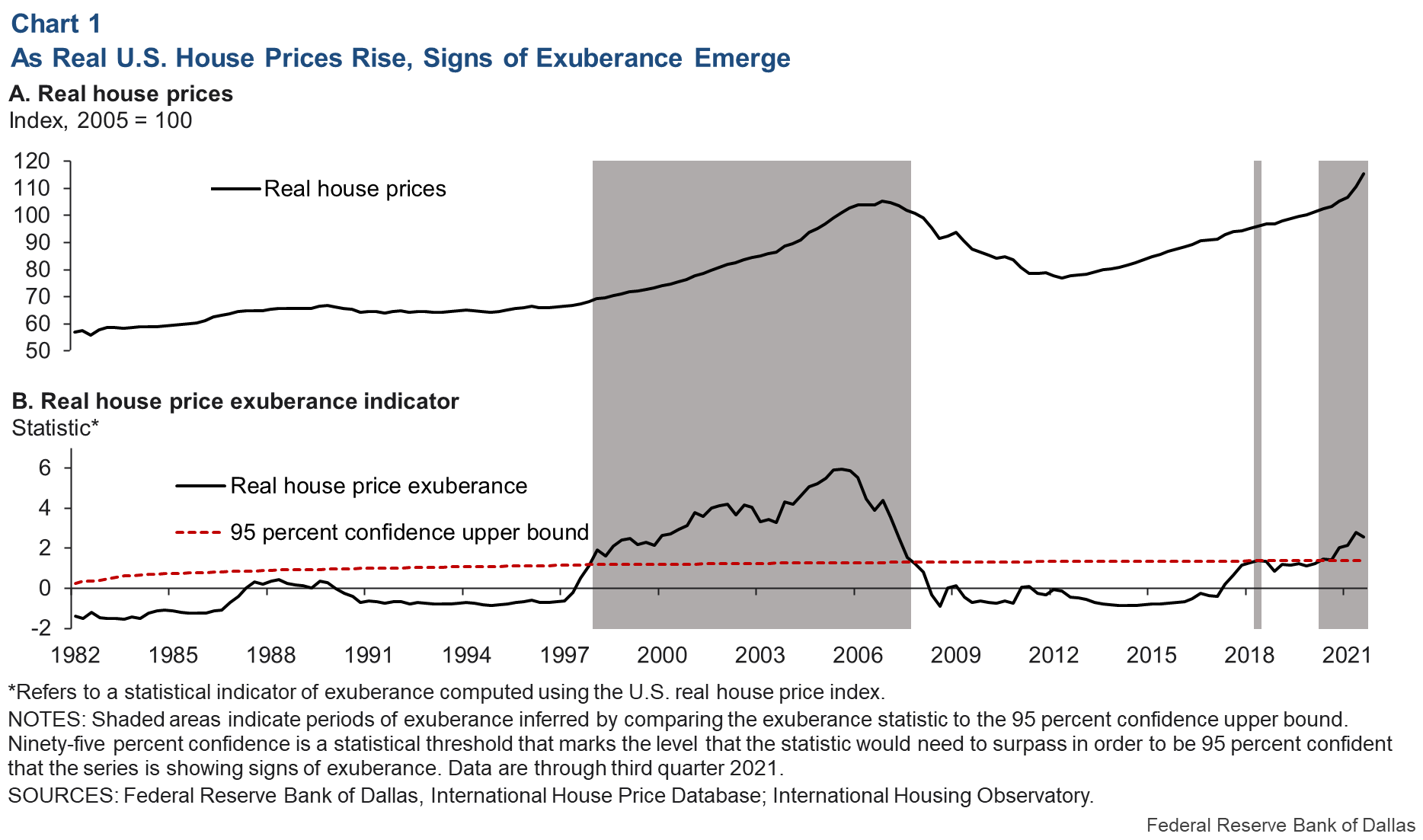

The researchers’ statistics show market “exuberance” — or when “prices are growing at an exponential rate exceeding what economic fundamentals would justify” — in both the 2000s and in 2021.

“The current reading indicates that the U.S. housing market has been showing signs of exuberance for more than five consecutive quarters through third quarter 2021,” researchers wrote.

The U.S. isn’t alone in this “housing market fever,” they noted. Eleven of 25 countries in their database show signs of exuberance.

What’s causing signs of a bubble?

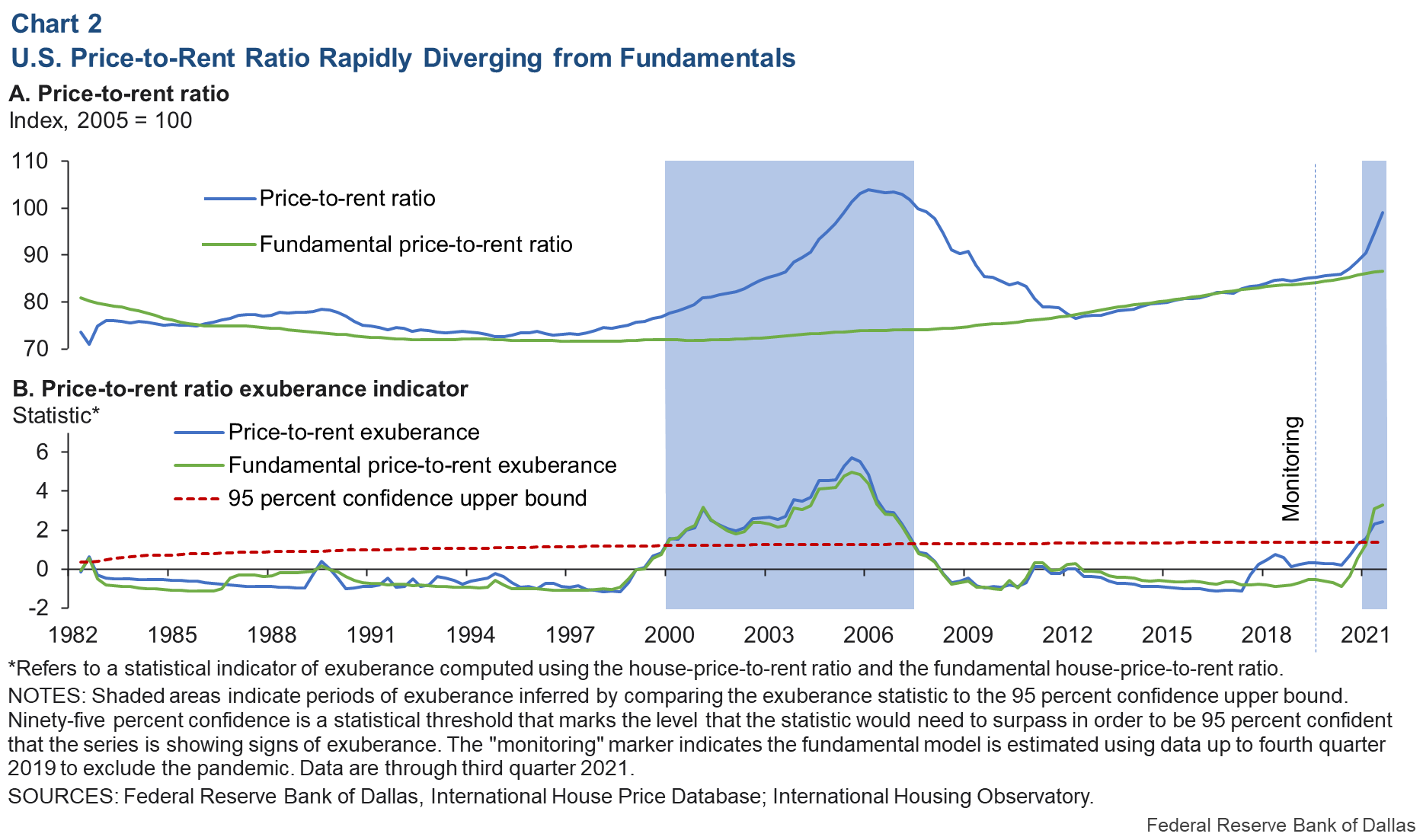

The researchers point to concerning price-to-rent ratios and price-to-income ratios.

{kind=link}

“Our evidence points to abnormal U.S. housing market behavior for the first time since the boom of the early 2000s,” researchers wrote. “Reasons for concern are clear in certain economic indicators — the price-to-rent ratio, in particular, and the price-to-income ratio —which show signs that 2021 house prices appear increasingly out of step with fundamentals.”

The researchers said historically low interest rates are a factor, but that they do not fully explain the U.S.’s housing market’s trends.

“Other drivers have played a role, including pandemic-related U.S. fiscal stimulus programs and COVID-19-related supply-chain disruptions and associated policy responses,” they wrote.

The resulting higher housing prices “may have fueled a fear-of-missing-out wave of exuberance involving new investors and more aggressive speculation among existing investors,” researchers wrote.

{kind=link}

Since the beginning of 2020, the price-to-rent ratio has “soared beyond what observed fundamentals alone can explain,” researchers said.

“The gap between the actual price-to-rent ratio and its fundamental-based level in the U.S. has grown rapidly during the pandemic — comparable to the run-up of the last housing boom — and started showing signs of exuberance in 2021,” researchers wrote. “The exuberance statistic confirms that recent increases are far from ordinary.”

Another important factor, researchers wrote, is the ratio of house prices to disposable income. Data showing “episodes of exuberance” for that ratio “do not yet display evidence of explosiveness in the third quarter of 2021.” However, researchers warned the “rapid increase in the statistic” in 2021 “indicates that U.S. real house prices may soon become untethered from personal disposable income per capita.”

That delay, researchers said, is partly because of a “surge” in disposable income during the pandemic that led to slower growth rates in the price-to-income ratio, mostly due to financial COVID-19 stimulus efforts and household spending reductions due to restrictions and cutbacks.

“If disposable income increases turn out to be transitory — as fiscal stimulus wanes and the Federal Reserve reverses its accommodative monetary policy — recent patterns in the price-to-income ratio may prove a less-useful measure of housing affordability,” researchers noted.