Andrew Asay said there are days when he’s so exhausted and anxious he doesn’t know how he’ll keep going.

“There have been a few points where my mind has just been racing. And I feel like just shutting down.”

The 27-year-old said he works two full-time jobs these days, one for a local mom and pop cabinet shop in Lindon, and one stocking shelves at Macey’s. Every weekday he works from 7 a.m. until 4 p.m. at the cabinet shop, then heads straight to Macey’s, where he works from 4:30 p.m. until 11 p.m. On Fridays and Saturdays, he works until midnight.

After work, he crashes as soon as he gets home. “And then I wake up in the morning and do it all over again. It’s kind of an endless cycle.”

It’s not that Asay doesn’t like the work — he’s grateful to have both of the jobs. But there are days when he’s running on fumes, and he feels like he has no choice but to hold both jobs in order to keep a roof over not only his own head, but over his entire family’s.

Asay’s mom, Deborah Koontz, is feeling the same anxiety. The 60-year-old mother is working full time at Walmart, and since she said they’ve not been allowing overtime she’s been considering taking on a second job. And her 22-year-old daughter, Asay’s sister Amanda, is also working two jobs to help contribute.

“We all need each other. I don’t think any one of us could do this without each other,” Koontz said, adding that she’s extremely proud of her children.

It’s barely enough, but they’re working hard to establish what they hope will be a better, more stable future for all three of them. And together, they’re in the final stages of moving away from renting to become homeowners.

But the family isn’t all that thrilled about making the purchase. Instead, their stomachs have been twisting in knots over it. But they feel like it was a decision that had to be made — not just for their futures, but also for a bit more added stability.

It’s a decision that Utahns across the state are having to make as housing prices — and rental rates — tick up to unfathomable heights. And as interest rates have climbed, especially over the past month, it’s added to the pain, forcing many to make excruciating decisions about whether to stretch their budgets even more — or walk away from the dream of homeownership.

Across the nation, including in Utah, home prices have been rising exponentially faster than American incomes. Plus, in recent weeks, as the Federal Reserve has upped the pressure in its war on inflation, the average rate for a 30-year mortgage topped 5%, some days topping the 6% threshold.

Combined with Utah’s high home prices, the over 5% rates have had a startling impact on Utahns: Over 70% have been priced out of the state’s median priced home, according to estimates by Dejan Eskic, senior research fellow with the University of Utah’s Kem C. Gardner Policy Institute, who specializes in housing research. Utah’s median home price shattered the $500,000 mark in February. That figure is even higher in Salt Lake and Utah counties.

The impact of these rising rates are what Eskic has described as “shocking.” In just one year, from April 2021 to April of this year, the median monthly mortgage payment skyrocketed by almost $1,000 from about $1,629 to $2,556 — a 56% jump.

And yet — while rising mortgage rates have cooled the market — some Utahns, like Asay and his family, are still stretching themselves to buy, equally frustrated by rising rental rates.

‘Barely making it’

Asay and his family, currently living in a three-bedroom apartment, were set this week to finalize a home loan to buy a $391,000 town house in Pleasant Grove. All three of them signed onto the loan to make it happen. Asay’s mother, Koontz, said she used all of her $15,000 in savings for the down payment. As of Friday, she said they were set to close on the loan.

Purchasing a home is no small milestone. But for Koontz, it doesn’t really feel like something to celebrate.

“You would think that buying a place, you should be all excited about it. But I’m not really excited about it. I’m kind of terrified,” she said. “I just hope that we can hang onto the place once we move in. I mean, if we lose it, I lose the $15,000 down payment I put on it. And that’s my savings. I’m going to be broke after all this goes through.”

Asay said he also feels squeamish about the whole thing. But at the same time, he said it felt like the best choice for their family — given that their current lease is about to expire and their landlord was about to jack their monthly price from about $1,800 a month to about $2,000 a month, including fees.

Considering Utah’s housing market and the direction housing and rental prices have been going — up, up, up — Asay said his family made the tough choice to spend the extra money now to lock themselves into an investment and hopefully insulate themselves from future rent price hikes that would catch them off guard.

So the three of them looked into buying a home. A single-family home was out of their price range. But they found a three-bedroom town house in a Pleasant Grove neighborhood that they were familiar with and liked.

Moving ahead with the loan process, the family got a bit of a gut punch when they saw the monthly payment would be over $2,300 with the 4.65% interest rate they qualified for. They questioned whether they should move forward.

“I actually wanted to back out of this whole deal,” Asay said. When I found out what the numbers were going to be, I was just like, ‘Ugh, I don’t think I can do this.’ Because we’d just barely be making it.”

But the thought of staying renters frustrated them. They were reluctant to pay nearly as much for a roof that wasn’t truly theirs all while remaining vulnerable to a landlord’s whims.

“If we continue to rent for a few hundred dollars less a month, I mean it’s still going to be painful because that money is basically going toward nothing. It would be like lighting it on fire,” Asay said. “At least the money you put into your mortgage — it might not be in your hands, but it will be in your house.”

Plus, if they didn’t lock in their rate when they did, that could have been the difference between paying even more a month. They were reading the writing on the wall, that the Fed was likely to bump up rates, and that could have broken their budget.

“It was a tough decision,” Koontz said, but they locked in their rate and pulled the trigger.

‘Something’s got to give.’ Will it?

To Koontz, the fact that a family of three working adults can barely scrape by to afford a three-bedroom town house is an indictment on Utah’s affordability crisis.

“One full-time job each isn’t enough,” she said. “It’s ridiculous. Something’s got to give. I guess we’re all waiting for that bubble to pop.”

If you talk to housing experts like Eskic, a 2006-like housing bubble burst is hard to fathom in today’s landscape. Leading up to 2006, risky lending practices enabled “everybody and their dog” to qualify for a home mortgage, as Eskic has put it, a time bomb that’s been depicted in films such as “The Big Short.” That helped feed a synthetic demand for housing that would eventually crumble as foreclosures caught up to big banks and the economy tumbled into the Great Recession.

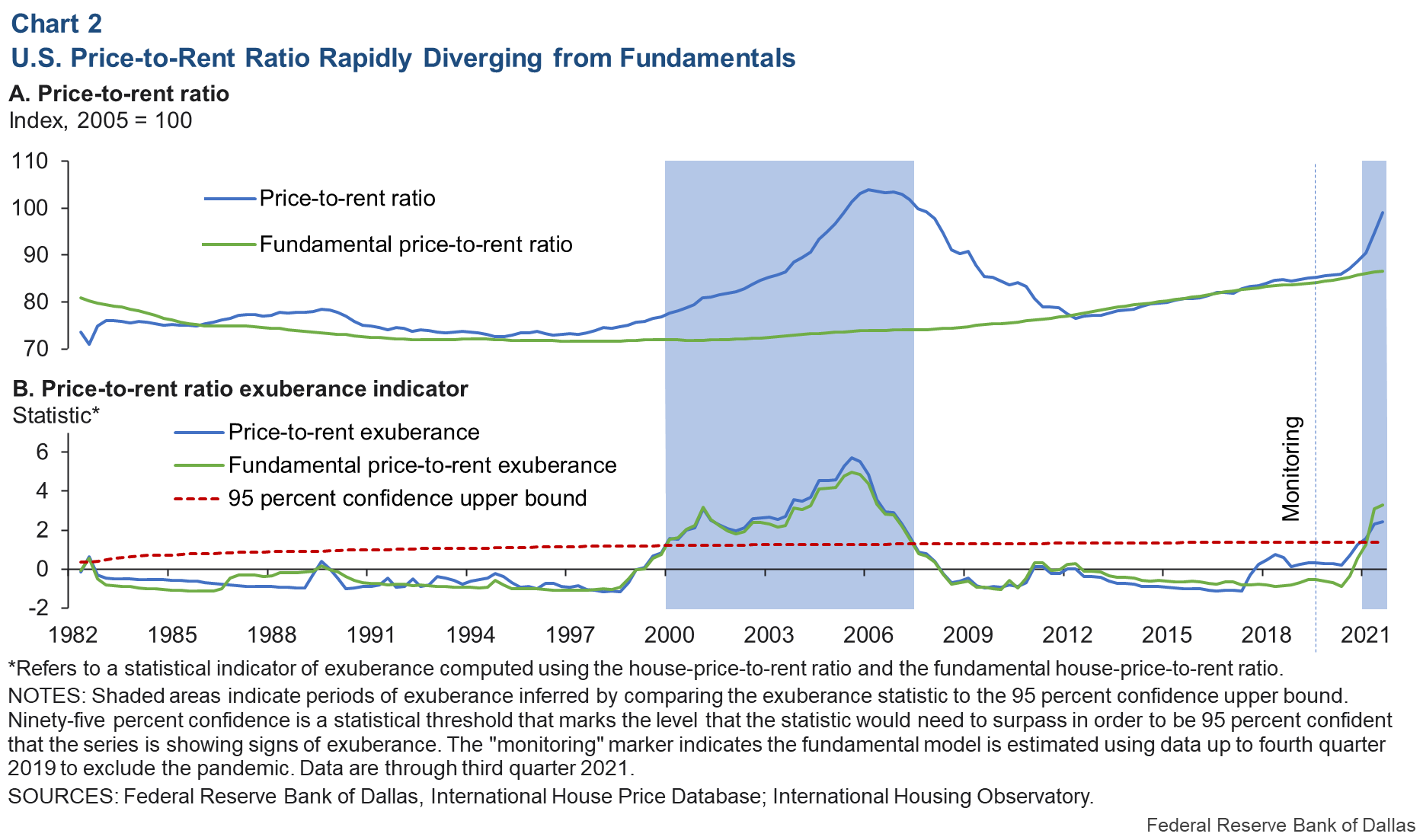

However, national housing researchers like those from the Federal Reserve Bank of Dallas have warned of a different type of bubble brewing, pointing to concerning price-to-rent ratios and price-to-income ratios showing that 2021 housing prices were increasingly out of step with market fundamentals.

{kind=link}

Still, housing experts note the U.S. — and Utah — remain in the throes of a real housing shortage. So demand for housing is real. That’s why it’s hard to fathom the same type of crash or bubble burst like we saw in 2007.

Today, it’s not easy to get a mortgage. But more Utahns than ever are stretched thin just to keep a roof over their head, whether it’s renting or maintaining a mortgage. Koontz wonders if or when this will catch up to the market in the form of foreclosures.

“That’s exactly what I worry about,” she said. “Once we move into this town home I’m really hoping we can make ends meet and not go into foreclosure. I’m scared to death about it. I stress out about it every day.”

The U.S. and Utah’s housing markets are contracting — and could be headed for at least slower home price growth compared to over the last two years, when prices skyrocketed amid the pandemic housing frenzy of the West. But that’s not the same as a crash or a bubble burst.

House prices likely won’t drop or plummet significantly unless Utah and the U.S. start to see massive layoffs, like what happened with the Great Recession, Dave Anderton, spokesman for the Salt Lake Board of Realtors, told the Deseret News.

“When people start losing their jobs and then they’re out of work, then we see home prices drop. But right now the job market’s pretty good. The best it’s been in a long time.”

As higher mortgage rates start to pinch and price out even more Utahns, more sellers in Utah have begun slashing their prices. The Provo market, in fact, saw the biggest percentage of price cuts in the nation in May, according to recent data posted by Redfin. Remember, though, listing price cuts aren’t the same as actual long-term price declines. Sellers often discount their prices if they’re motivated to sell or if they’re finding their initial list price was out of step with what buyers are actually willing to pay.

A better indicator if the housing market is actually going to see prices fall is if the market sees at least 18 months of falling sales, Anderton said. As of June, Utah has seen 11 months of falling sales as inventory has lagged and mortgage rates squeeze buyers.

“If we have another six months (of falling sales) then I think you’re going to see that reflected” in the data, Anderton said. If enough sellers drop their prices for a long enough period of time, then actual price drops will begin showing up in official sales price data.

Still, that’s after more than two years of double-digit price increases, amounting to an increase of 50% to Salt Lake’s home prices since 2020, according to the Salt Lake Board of Realtors.

“That’s a huge run-up in prices, so even if prices dip a little bit the average buyer won’t feel it,” Anderton said. Meanwhile, the economy remains fairly strong, even though inflation is pinching people. “There’s still demand, still people moving here, still a good economy, a lot of jobs. So the market is fairly good, it’s just going to be more difficult for people who need a mortgage to pay for a high price of a home and high interest rates.”

Buyers are walking away

Other than homebuyers, mortgage companies have been among the first to feel the sting of climbing mortgage rates. Real estate giants like Redfin, Compass and mortgage lender JPMorgan Chase & Co. have started laying off employees as U.S. mortgage applications have fallen to the lowest level in 22 years, as the Wall Street Journal reported.

Anderton’s brother, Rick Anderton, owns Ridge Home Loans, a mortgage company based in Pleasant Grove that serviced Asay’s and his family’s mortgage. He said his company is feeling the pinch from the slowdown, but he expects it to weather it, noting he knew “we were borrowing from the future” when mortgage rates were low.

“At some point you have to pay for that because there has to be a retraction,” he said. “And now we are.”

Rick Anderton is on the front lines with aspiring homebuyers. He’s there with them when they’re trying to make the hard decision to buy or walk away. As rates have ticked up — combined with inflation — those choices are only getting more painful.

“They feel squeezed,” he said. “I had one client go through their budget and add up all their expenses. They said their monthly expenses have gone up $600 a month for food, gas and just living expenses. And so they’re deciding whether to back out of their home purchase, under contract with a builder.”

Rick Anderton said there are certainly buyers who are walking away from their contracts, especially if they waited to lock until after rates jumped. “I don’t think the majority, but it definitely feels like we hit a price point where people are questioning, reconsidering their contracts.”

“It feels to me that we’ve hit the resistance with price and rates, where it’s just unsustainable.”